【Cross Border-Search】 has provided precise business intelligence to over 10,000 enterprises based on authoritative customs data. Our business spans the entire foreign trade industry chain, including global trade solutions, CRM systems, and digital marketing services.

To request a free trial or learn more about how Cross Border-Search can empower your business, please feel free to send us a private message!

I. Insights into Customs Data Platform Demand Amid the Foreign Trade Digitalization Wave

In the first quarter of 2026, China’s battery exports (HS Code 8507) exhibited an unprecedented structural divergence. While traditional markets like Germany and the United States faced a “deep freeze,” emerging sectors such as the Netherlands, Australia, India, and Central and Eastern Europe experienced explosive growth. This shift is not merely a natural migration of market demand; it is the result of the combined impact of global green trade barriers, geopolitical maneuvering, and domestic industrial upgrades.

Based on the latest 2026 export customs data and policy environment from Cross Border-Search, this article provides a deep dive into the industry scope of HS Code 8507 and analyzes the current shifts in the global foreign trade landscape.

I. Which Industries Does HS Code 8507 Cover?

HS Code 8507, internationally recognized as “Electric Accumulators (Storage Batteries),” primarily encompasses the following sectors:

- Lead-Acid Batteries: Used for automotive starting, UPS power supplies, telecommunication base stations, and low-speed electric vehicles (LSEVs).

- Lithium-ion Batteries: Includes power batteries (EVs), energy storage systems (utility-scale power plants, residential storage), and consumer electronics batteries (smartphones, laptops, etc.).

- Nickel-Metal Hydride (NiMH), Nickel-Cadmium (NiCd), and Other Batteries: Applied in industrial equipment, medical instruments, and specialized tools.

Within China’s export structure, the core growth engine for HS 8507 has already shifted from traditional lead-acid batteries to lithium-ion batteries. Specifically, power batteries and Energy Storage Systems (ESS) have become critical pillars of the “New Three” (electric vehicles, lithium-ion batteries, and solar products) export categories.

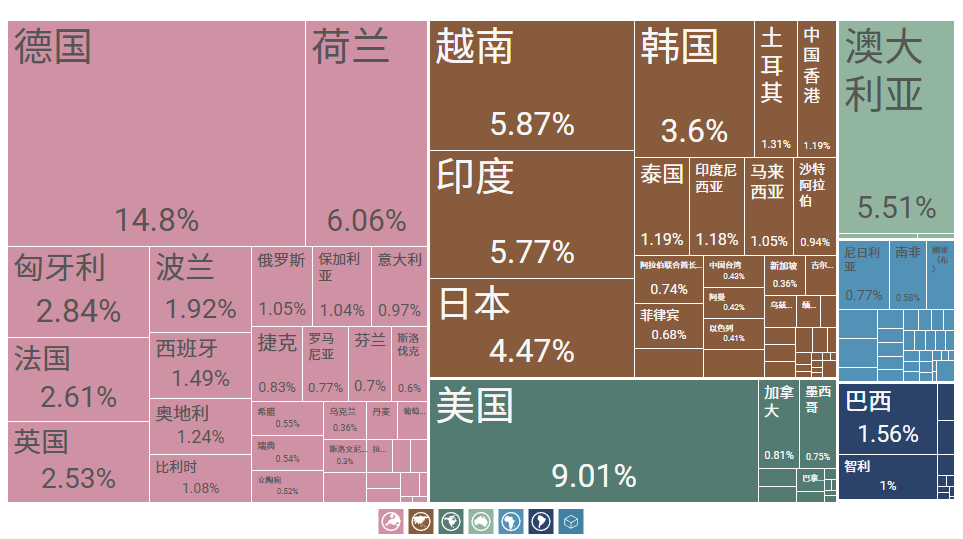

II. Q1 2026 Export Data Overview: A Tale of Fire and Ice

Source: Cross Border-Search Big Data Inquiry Platform

1. Traditional Anchor Markets “Losing Momentum”

- United States: Export value plummeted by -58.61% year-on-year (YoY), with its market share dropping to 9.01%. The primary drivers are the increased localization requirements of the Inflation Reduction Act (IRA) and the full implementation of Section 301 tariffs, which have directly obstructed direct export routes to the U.S.

- Germany: Exports declined by -24.33% YoY. While it remains the largest export market (14.81% share), the EU New Battery Regulation and the hidden carbon costs of CBAM (Carbon Border Adjustment Mechanism) are rapidly squeezing out enterprises with low compliance capabilities.

2. High-Value Markets “Exploding”

- Australia: Surged by +92.53% YoY, with an average unit price (AUP) reaching $237.68, reflecting robust demand for large-scale Energy Storage Systems (ESS) and high-end industrial batteries.

- Netherlands: Increased by +48.08% YoY, with an AUP of $85.93, solidifying its strategic status as the “European New Energy Transit Hub.”

- Central and Eastern Europe (CEE): Growth rates in Austria (+215.05%), Bulgaria (+138.18%), and Poland (+56.67%) were staggering. This trend highlights how Chinese battery manufacturers are driving exports of equipment and materials through their overseas factories in regions like Hungary and Poland.

3. Extreme Divergence in Scale and Pricing

- India: Accounted for 19.17% of export volume, up +13.33% YoY. However, the AUP was only $4.79, characterizing a market that is “high volume, low price, but steadily upgrading.”

- Vietnam: Represented 19.11% of export volume with an AUP of just $4.89, primarily serving low-end assembly and entrepôt trade functions.

The price spectrum—ranging from $4.79 to $306.76—clearly reveals that Chinese battery products have developed a highly stratified competitive edge: high-volume exports at the low end, quality stability in the mid-range, and systematic solution exports at the high end.

III. Underlying Policy Logic: Who is Reshaping the Export Landscape?

1. United States: The “Double Blow” of Tariffs and Localization

- Inflation Reduction Act (IRA): In 2026, the domestic content requirements for battery critical minerals and components have tightened further. The threshold for battery components manufactured or assembled in North America has risen to 70% to qualify for full tax credits.

- Section 301 Tariffs: The 2024-2026 tariff hikes on strategic sectors are now in full effect. Notably, as of January 1, 2026, the tariff rate on non-EV lithium-ion batteries (including energy storage and consumer electronics) has officially jumped from 7.5% to 25%.

- Policy Volatility: Following preliminary anti-dumping/countervailing duty (AD/CVD) rulings in early 2026, combined with the restart of specific Section 301 investigations, U.S. importers have largely adopted a “wait-and-see” approach, leading to widespread order delays or cancellations.

2. European Union: Green Barriers Forcing Supply Chain Restructuring

- New Battery Regulation (EU 2023/1542): 2026 marks the move from roadmap to enforcement. As of February 18, 2026, mandatory carbon footprint declarations for industrial batteries are live. Furthermore, by August 18, 2026, enhanced labeling requirements regarding capacity, lifespan, and chemical composition become compulsory.

- Digital Battery Passport: While the mandatory QR-code-based Battery Passport for EV and industrial batteries (>2 kWh) officially starts on February 18, 2027, 2026 is the critical “sync year” where manufacturers must finalize data integration.

- CBAM (Carbon Border Adjustment Mechanism): Although batteries aren’t the primary target, the indirect carbon costs from steel and aluminum casings are creating price pressure. Enterprises without robust carbon accounting face an effective “green tax” that can add significant overhead.

These policies have effectively squeezed Chinese firms with low compliance capabilities out of core markets like Germany. Conversely, Central and Eastern Europe (e.g., Hungary and Poland) has emerged as a new “springboard” for exports to the EU, driven by the operational launch of overseas factories by leading Chinese battery giants.

3. China Domestic: Elimination of Export Tax Rebates Driving Industrial Upgrading

- April 1, 2026: The export tax rebate rate for batteries has been reduced from 9% to 6%.

- January 1, 2027: The value-added tax (VAT) export tax rebate for battery products will be completely abolished.

This phased exit policy sends a clear signal: “Anti-internal competition (anti-neijuan), Pro-upgrading.” While it triggered a short-term “export rush” in Q1 2026 as companies raced against the April deadline, its long-term impact will be the accelerated elimination of low-end overcapacity. This policy shift forces Chinese enterprises to pivot toward high-end value chains, green manufacturing, and globalized operations.。

IV. Strategic Roadmap: “Battle Map” for Battery Exporters in 2026

Strategy 1: Pivot from “Product Export” to “Ecosystem Globalization” in Western Markets

- Targeting the U.S.: Shift away from direct exports. Focus on LRS (Licensing, Royalty, and Service) models, equipment output, and joint venture manufacturing. Alternatively, utilize compliant regional hubs such as Mexico or Southeast Asia for localized assembly.

- Targeting the EU: Embed supply chains into CEE nodes like Hungary and Poland, while establishing marketing and after-sales hubs in the Netherlands or Germany. Completing Carbon Footprint Certification and Battery Passport integration is no longer optional—it is a core competitive advantage.

Strategy 2: Market Stratification—Moving Beyond a “One-Size-Fits-All” Approach

- Premium High-Value Markets (Australia, Austria, Japan): Prioritize utility-scale Energy Storage Systems (ESS), marine propulsion, and medical-grade batteries. Transition from selling components to delivering comprehensive system-level solutions.

- Scalable Emerging Markets (India, Indonesia, Vietnam): Shift from exporting low-end finished goods to becoming an “infrastructure provider.” Export production line equipment, cathode/anode materials, and technical standards.

Strategy 3: Focus on Absolute Growth Pools

Strategically allocate resources to markets showing simultaneous growth in both volume and value, such as Poland, Hungary, Indonesia, and Brazil. These regions are either absorbing industrial spillovers from developed nations or are in the early stages of a massive New Energy infrastructure boom.

Strategy 4: Establish Risk “Circuit Breaker” Mechanisms

For markets with high volatility or heavy reliance on entrepôt trade (e.g., Saudi Arabia, South Korea, Hong Kong SAR), implement a dual-verification system of “Data Alerts + Policy Research.” Proactively undertake strategic contractions where necessary to mitigate bad debt risks arising from sudden geopolitical shifts.

Conclusion

The Q1 2026 export data for HS Code 8507 represents a “watershed moment” for the global expansion of China’s battery industry. It signals the end of an era of extensive, unrefined growth, while clearly illuminating the path forward:

The winners of the future will no longer be those who can sell batteries at the lowest price. Instead, victory belongs to those who can successfully navigate the complexities of carbon barriers, tariff walls, and localization compliance to build an irreplaceable global industrial niche.

Moving products up the value chain, expanding market footprints globally, and deepening business models—this is not just a strategy to manage change; it is the only path toward the next stage of high-quality development.

*The data in this article is based on statistics from the Cross Border-Search Big Data Inquiry Platform and is for reference only. Markets involve risks; strategic planning should be approached with caution.